Where Have Colorado's Construction Workers Gone?

Examining Colorado's recent job loss in the construction industry and the significance of wages as a meaningful factor

According to estimates from the Current Employment Statistics (CES) program, Colorado’s employment growth in the construction industry ranks as one of the worst in the nation. Over the past year (June 2023 to June 2024), Colorado has shed 4,200 construction jobs, on a seasonally adjusted basis, which translates to a growth rate of -2.3%. Only Maryland and Maine have worse construction job growth rates over that period. Compared to two years ago, Colorado is just one of six states with job loss in construction, with an employment decrease of 2,000 and a related growth rate of -1.1% (comparatively, U.S. construction jobs have grown by 6.2%). Additionally, Colorado has experienced declines in construction employment in 12 of the past 24 months, the highest rate of monthly job loss over a two-year period for the state since the Great Recession. Given the importance of the industry in fulfilling present and future infrastructure and housing needs, it is worth examining potential drivers for Colorado’s lackluster job growth in construction. Specifically, this article will look at construction wages in Colorado as well as some longer-term employment trends.

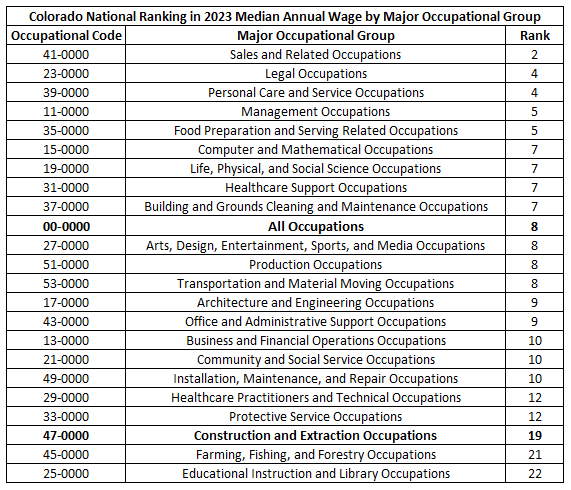

Due to a number of factors (like demographics, industry mix, and cost of living), Colorado is a high-paying state, with wages that outpace much of the nation. For instance, Colorado had the 6th highest private sector average hourly earnings in 2023, per CES estimates. Similarly, the state’s average weekly wage of $1,483 last year ranked 7th nationally, based on data from the Quarterly Census of Employment and Wages. However, the state’s wage competitiveness lags when it comes to construction. Using the same datasets from above, Colorado ranked 16th and 15th, respectively, in average wages paid within the construction industry. While comparing industry-level wages definitely has value, data from the Occupational Employment and Wage Statistics (OEWS) program allows for more detailed analysis. The table below displays Colorado’s national ranking in 2023 median annual wage for all occupations and 22 major occupational groups. While the state’s median annual wage for all occupations ranked 8th last year (and 17 major occupational groups had top 10 ranks), the construction and extraction occupational group (which includes mining jobs) only ranked 19th. Notably, the gap in Colorado’s median wage ranking between all occupations and the construction and extraction group can be observed going back to the early 2000s, as the following chart shows.

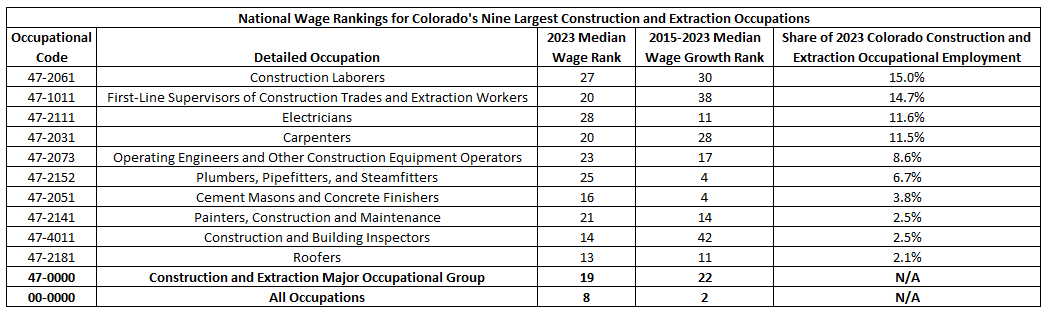

While those broad occupational rankings basically align with the previously mentioned industry trends, drilling down to detailed occupations within construction reveal varying levels of wage competitiveness weakness and limited areas of upside. The subsequent table focuses on the nine largest construction occupations in Colorado (which account for 79% of total construction and extraction occupational employment in the state) and presents two different sets of wage rankings: 1) respective national ranks in 2023 median wage; and 2) respective national ranks in median wage growth from 2015 to 2023, which borrows from a concept explored in a previous article. Construction laborers, which represented 15% of Colorado’s construction and extraction occupational employment in 2023, had the 27th highest median wage in the U.S. last year and fared even worse (30th) in wage growth over the past eight years. This is in stark contrast to Colorado’s respective rankings of 8th and 2nd for all occupations. The second largest occupation, supervisors of construction and extraction workers, faces a similar issue, with a median wage ranking of 20th and wage growth that ranks within the bottom third nationally. While there are some exceptions of an occupation ranking in the Top 15 either in 2023 median wage or 2015 to 2023 wage growth, only roofers (2.1% of Colorado construction and extraction occupational employment) exhibit relative strength in both rankings.

So why is any of this important or worth mentioning? In a labor market, wages are one key component in attracting and retaining workers. This point became glaringly obvious in the years following the pandemic, as the quits rate exceeded historic highs, job switchers were rewarded with faster gains in wages compared to those who remained in their old job, and inflation reached a 40-year peak. Although labor market tightness has subsided over the past year, there is still a heightened level of competition for workers within and between states, depending on the industry and occupation. And while relatively high-paying and competitive wages are generally demonstrated in Colorado, the same cannot be said regarding construction earnings within the state. It’s possible that this long-term trend in comparatively mediocre wages in construction is now impacting Colorado from an employment standpoint, with these physically demanding jobs become harder to fill as the importance of pay rates is elevated. Potential construction workers may instead look for other similar work outside of Colorado or jobs within the state that are in an entirely different industry or occupation.

In an effort to support the claim made in the last sentence, the following three charts utilize a rich source of data from the U.S. Census Bureau that track quarterly industry job flows by state (technical documentation and data for these job flow statistics are available within the Longitudinal Employer-Household Dynamics website). While this dataset is lagged by a year (the most recent data is currently from second quarter 2023), it is unmatched with the level of information available on worker mobility. The first chart features data that focuses on a subset of construction workers who switch jobs, but remain in construction, and whose new geographic location of employment is either from Colorado to a different state or vice versa (other methodological detail is provided within the chart caption below). Essentially, this can be viewed as a proxy of construction workers who move (or “flow”) to and from the state, and whether the net change for Colorado is positive or negative. What shows is a series of periods where Colorado’s net change alternates between negative and positive. The most notable net positive spike occurred between 2012 and 2014, which also coincided with the height of the oil and gas/fracking boom in the state, while the past two recessions (2009-10 and 2020) featured the largest net negative changes for Colorado. Through the most recent four-quarter period available (Q3 2022 to Q2 2023), Colorado’s net change is slightly negative. While the net flow counts have historically bounced between negative and positive, the newest data extends a persistent trend of negative (or near zero) job flows for the state.

The next chart utilizes the methodology from above, but instead looks at the aggregate net job flows for all industry sectors, excluding construction (specifically, this graph adds up same industry net flows – so manufacturing-to-manufacturing, retail trade-to-retail trade, etc. – between Colorado and other states for each four-quarter period). Contrary to the preceding construction graphic, this chart presents a net flow that is consistently positive for Colorado since 2005, which translates to job gains for the state when observing worker movement within these combined industry sectors. This trend is significantly more aligned with data that shows Colorado as a state with historically positive net migration population growth, when compared to the construction industry job flow chart.

The final chart displays net job flows within Colorado and the movement to and from construction to other industry sectors. Interestingly, aside from the Great Recession, these net job flows have been positive for construction. However, that advantage has notably eroded over the past several years. This could possibly indicate that workers may view construction as a relatively less attractive option when switching jobs/industries within Colorado.

While there could certainly be other factors to help explain Colorado’s disappointing performance in recent construction employment growth, the role of wages should not be discounted or underestimated. As mentioned at the beginning of this article, the construction industry is instrumental in meeting local, state, and national demands for additional housing and improved infrastructure, and competition for that labor should remain robust for the foreseeable future. Hopefully Colorado can begin to reverse the trend of relative wage weakness in construction, or the state might continue to find itself lagging the nation in filling these crucial jobs.

Thrilled to discover your work. Really interesting look at construction employment. I'm curious whether the passage of statewide prevailing wage and the expansion of more minimum wages in several metro Denver communities will have positive impacts on construction wages over time? Most construction wages are well-above minimum in the skilled trades, but more of which are likely to hover closer to minimum for basic crafts especially in the lower density residential sectors of construction, and as wages in these sub-markets rise compression could result in increases even for those earning above the minimum. Given the state's budget they may not be a large enough purchaser of construction labor to influence the overall market, but that is the theory that motivates prevailing wage policy...